How Do TOD, TOM, and SPT Contracts Differ Mechanically?

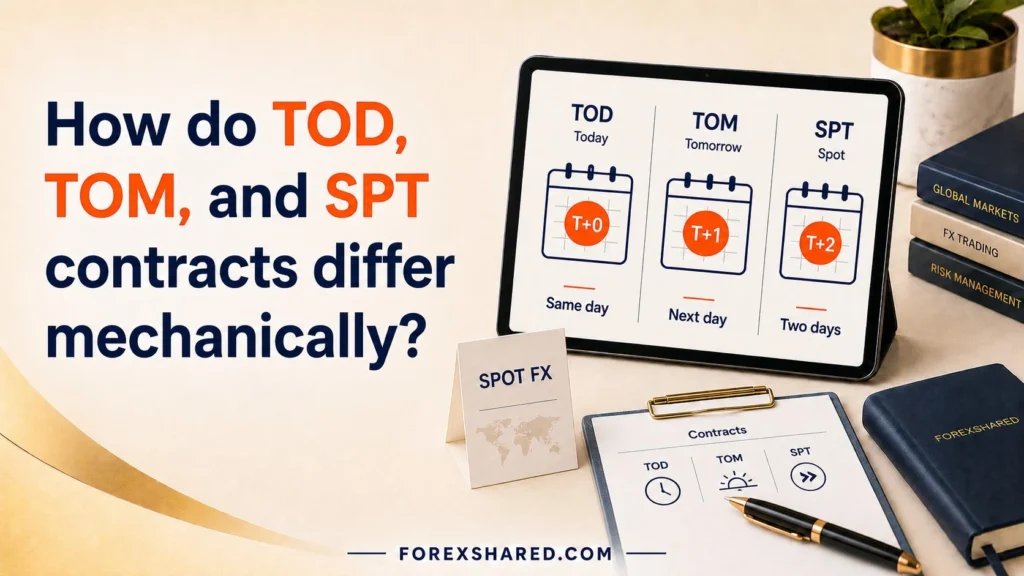

TOD, TOM, and SPT contracts differ mechanically by settlement timing. TOD settles on the trade date, TOM settles on the next business day, and SPT follows the standard spot value-date structure.

The core difference is not the currency pair itself, but the value date attached to the contract. The same currency pair can appear under different settlement codes depending on whether delivery is scheduled today, tomorrow, or on the standard spot date.

This article explains how TOD, TOM, and SPT work, how their value dates differ, how pricing and settlement mechanics change, how business-day calendars affect them, and which contract terms confirm the correct classification.

This article is for educational purposes only. It does not provide trading advice, investment advice, settlement advice, broker recommendations, leverage guidance, position-size guidance, order-type guidance, or live execution instructions.

What do TOD, TOM, and SPT mean in FX contracts?

TOD, TOM, and SPT are FX settlement-timing labels that describe whether value date is today, tomorrow, or the standard spot date.

TOD usually means Today or Value Today. TOM usually means Tomorrow or Value Tomorrow. SPT usually means Spot or Value Spot. These labels describe settlement timing, not currency-pair identity. Recognizing these variations is a fundamental part of understanding spot settlement exceptions across the institutional landscape.

What does TOD mean?

TOD refers to a same-day value-date contract. Trade date and value date are exactly the same day, compressing the entire settlement process into hours rather than days. Citi describes Value Today as a transaction where both trade date and value date are today. [Citi, FX Transactions]

What does TOM mean?

TOM refers to a next-day value-date contract. Settlement is officially scheduled one business day directly after the initial trade date. Citi separates Value Tomorrow from Value Today and Value Spot, showing next-day settlement as a distinct FX timing structure. [Citi, FX Transactions]

What does SPT mean?

SPT refers to a standard spot value-date contract. Value Spot commonly means final settlement strictly occurs on the second business day immediately after the trade date. Citi defines Value Spot as settlement on the second business day from the trade date. [Citi, FX Transactions]

TOD, TOM, and SPT are FX settlement-timing labels: today, tomorrow, and standard spot.

How does value date create the mechanical difference?

Value date creates the mechanical difference because it confirms whether the contract settles today, tomorrow, or on the standard spot date.

The explicit value date is mathematically significantly more important than the brief shorthand label alone. The exact same currency pair can readily appear across multiple platforms under entirely different settlement codes. The designated value date rigorously controls whether the contract is genuinely same-day, next-day, or standard spot.

| Contract Code | Plain Meaning | Settlement Timing | Mechanical Role |

|---|---|---|---|

| TOD | Today | Trade date | Same-day settlement |

| TOM | Tomorrow | Next business day | Next-day settlement |

| SPT | Spot | Standard spot value date | Usually T+2 baseline |

| Trade Date | Deal date | Start of timing count | Price and terms agreed |

| Value Date | Settlement date | Final delivery target | Contract timing confirmed |

Why is value date more important than the label?

Value date is more important than the label because it proves the actual settlement date. TOD, TOM, and SPT are shorthand labels, but the value date formally confirms the settlement mechanics. FX settlement timing is commonly described through trade date and settlement/value date concepts. [Chicago Fed, 2006]

How does the same pair appear under different codes?

The same pair can appear under different codes when the delivery date changes. The pair remains the same, but the value date changes to meet the participant’s exact liquidity need. Moscow Exchange lists FX instruments using codes such as TOD, TOM, SPT, TOD/TOM, and TOM/SPT. [Moscow Exchange, FX Instruments]

What does the value date control mechanically?

The value date controls when settlement is scheduled. It explicitly controls exactly whether the active contract is executed as same-day, next-day, or standard spot. Furthermore, it can radically also affect overarching pricing mechanics because the timing offset logically can include a significant time-value or swap-interest adjustment.

The mechanical difference between TOD, TOM, and SPT is the value date.

How does a TOD contract work mechanically?

A TOD contract works mechanically as a same-day settlement structure where trade date and value date are the same.

TOD essentially functions as Value Today or T+0 settlement. By design, TOD dramatically compresses the traditional settlement cycle directly into the initial trade date. Consequently, operational pressure is remarkably highest because massive funding logistics and complex payment instructions absolutely must be completely ready incredibly quickly. Exploring TOD contract restrictions systematically highlights why widespread usage is impossible without proper institutional readiness.

| TOD Element | Mechanical Meaning |

|---|---|

| Contract Label | TOD or Value Today |

| Trade Date | Today |

| Value Date | Today |

| Settlement Gap | T+0 |

| Operational Pressure | Highest because settlement is same-day |

| Main Use Case | Immediate or urgent currency delivery |

What is the settlement timing of TOD?

TOD settlement timing is T+0. The financial contract is rigorously scheduled to fully settle on the exact same day it is initially agreed. Panin describes Today as foreign-exchange purchase or sale where the delivery date equals the transaction date. [Panin, Today Tomorrow Spot]

Why does TOD create more operational pressure?

TOD creates more operational pressure because same-day settlement leaves less time for funding and settlement instructions. The strict daily cut-off time, instant funding readiness, immediate account access, and overlapping banking availability matter massively more for TOD transactions. If instructions are delayed, the trade can completely fail.

What can stop TOD from being practical?

Late execution, currency holidays, and missing payment instructions can make TOD difficult to settle. Successful same-day settlement inherently requires perfectly valid, simultaneous settlement access across both sovereign currency jurisdictions. Debilitating currency holidays or awkwardly late cut-off times can effortlessly make same-day processing practically impossible to finalize.

TOD is mechanically the shortest settlement structure because trade date and value date are the same.

How does a TOM contract work mechanically?

A TOM contract works mechanically as a next-business-day settlement structure where value date falls one business day after trade date.

TOM universally represents Value Tomorrow or precise T+1 execution timing. This specialized structure effectively creates a one-day operational buffer. Therefore, TOM logically gives participants marginally more time than highly compressed TOD execution, but significantly less time than standard SPT timing.

| TOM Element | Mechanical Meaning |

|---|---|

| Contract Label | TOM or Value Tomorrow |

| Trade Date | Today |

| Value Date | Next business day |

| Settlement Gap | T+1 |

| Operational Pressure | Lower than TOD but tighter than SPT |

| Main Use Case | Near-immediate but not same-day settlement |

What is the settlement timing of TOM?

TOM settlement timing is T+1. The specific currency trade is mathematically agreed today, but actual physical settlement is officially scheduled exactly for the next valid business day. Panin describes Tomorrow as FX delivery made one business day after the transaction date. [Panin, Today Tomorrow Spot]

How is TOM different from TOD?

TOM differs from TOD because TOM settles on the next business day while TOD settles on the trade date. The critical one-business-day gap generously gives participants significantly more operational time than a restrictive TOD trade. This extra twenty-four hours massively reduces the dangerous friction associated with missing strict daily cut-off times.

How is TOM different from SPT?

TOM differs from SPT because TOM settles earlier than the standard spot value date. The SPT contract usually safely uses the universally standard spot value date, which is typically two days out. Citi separates Value Tomorrow from Value Today and Value Spot, showing next-day settlement as a distinct FX timing structure. [Citi, FX Transactions]

TOM is mechanically a next-business-day contract that sits between same-day TOD and standard SPT.

How does an SPT contract work mechanically?

An SPT contract works mechanically as the standard spot value-date structure rather than a same-day or next-day contract.

SPT serves dynamically as the baseline Value Spot reference point globally. For the vast majority of major FX transactions, standard spot settlement is commonly firmly anchored exactly at T+2. This foundational timeline provides the maximum operational flexibility allowed within the short-dated spot category, efficiently separating immediate pricing from complex logistical delivery mechanics.

| SPT Element | Mechanical Meaning |

|---|---|

| Contract Label | SPT or Value Spot |

| Trade Date | Today |

| Value Date | Standard spot date |

| Settlement Gap | Often T+2 for many pairs |

| Operational Pressure | Lower than TOD and TOM |

| Main Use Case | Standard spot settlement |

What is the settlement timing of SPT?

SPT refers to the standard spot settlement structure. Standard spot settlement is most commonly mathematically described accurately as physically occurring on the second valid business day directly from the trade date. Citi defines Value Spot as settlement on the second business day from the trade date. [Citi, FX Transactions]

Why is SPT not always literal same-day delivery?

SPT is not literal same-day delivery because it uses the spot value date. The formal price execution may safely be agreed completely today while actual physical settlement is officially scheduled precisely for the subsequent spot value date. Spot means near-term settlement, not necessarily immediate instantaneous delivery.

Why can SPT settlement still shift?

SPT settlement can still shift because business-day rules and currency holidays can adjust the final value date. Intervening weekends and unpredictable sovereign currency holidays absolutely can significantly affect overarching spot settlement-date calculations. CME’s EBS value-date calendar material treats weekends and currency holidays as factors in spot and forward settlement-date calculations. [CME Group, EBS Value Date Calendar]

SPT is mechanically the standard spot-value contract, usually longer than TOD and TOM.

How do TOD, TOM, and SPT differ in settlement timeline?

TOD, TOM, and SPT differ in settlement timeline by settlement gap: T+0, T+1, and standard spot timing.

This distinct separation creates a clear, cascading timeline. Each specific structure sequentially adds exactly one additional valid business day of operational padding between the initial price execution and the final currency exchange.

| Day | TOD | TOM | SPT |

|---|---|---|---|

| Trade Date | Trade and settle | Trade date | Trade date |

| Next Business Day | Already settled | Settlement date | Waiting period |

| Second Business Day | Already settled | Already settled | Typical spot settlement date |

| Timing Code | T+0 | T+1 | Often T+2 |

| Main Difference | Same-day | Next-day | Standard spot |

Which contract settles fastest?

TOD settles fastest because it targets same-day settlement. It undeniably is the absolute shortest value-date structure actively available in the institutional market. TOD is incredibly more sensitive specifically to strict daily cut-off times and immediate operational readiness. A failure to execute perfectly on the trade date results in an immediate settlement failure.

Which contract sits in the middle?

TOM sits in the middle because it gives one business day between trade and settlement. TOM is decisively shorter than the standard spot cycle but remarkably less urgent than demanding same-day delivery. It perfectly bridges the frantic urgency of TOD and the relaxed baseline of SPT.

Which contract uses standard spot timing?

SPT uses standard spot timing. For many major, heavily traded FX pairs, this practically means a reliable second-business-day value date. Citi’s Value Spot definition supports settlement on the second business day from trade date. [Citi, FX Transactions] It is the default structure driving the vast majority of non-urgent global currency flows.

TOD, TOM, and SPT differ mechanically by settlement gap: T+0, T+1, and standard spot timing.

How does pricing differ across TOD, TOM, and SPT?

Pricing can differ across TOD, TOM, and SPT because each contract uses a different value date and settlement window.

The explicit value-date difference means the provided quotes are absolutely not interchangeable. Capital has a time value, and altering the delivery date actively alters the internal math required to execute the transaction efficiently.

| Pricing Layer | TOD | TOM | SPT |

|---|---|---|---|

| Base Rate Reference | Same-day FX rate | Next-day FX rate | Spot FX rate |

| Timing Adjustment | Can reflect same-day funding conditions | Can reflect one-day adjustment | Standard spot benchmark |

| Liquidity Effect | May depend on same-day availability | May depend on next-day availability | Often deeper standard spot market |

| Operational Cost | Higher urgency | Moderate urgency | Standard settlement window |

| Reader Risk | Assuming all three use the same rate | Ignoring time-value adjustment | Treating spot as instant delivery |

Why can the rates differ?

The rates can differ because TOD, TOM, and SPT have different settlement dates. The shorter settlement timing can actively influence the final all-in rate presented to the user. Citi notes that Value Today and Value Tomorrow can be made with settlement on the same day or next day while factoring swap interest rate into the price. [Citi, FX Transactions] This structural adjustment accounts for the cost of advancing or delaying capital.

Why does TOD not always equal SPT?

TOD does not always equal SPT because same-day settlement can have different funding and pricing treatment. TOD aggressively settles significantly earlier than the standard SPT baseline. Because the dealer must provide immediate, high-priority liquidity, the all-in rate can dynamically shift to reflect the heightened urgency.

Why does TOM not always equal SPT?

TOM does not always equal SPT because TOM settles earlier than standard spot. The one-day mathematical differential dictates that a slight pricing adjustment may accurately apply to balance the funding timeline. Therefore, the specific contract definitively should be read rigorously by its value date and actual all-in price, not solely by the generic pair name.

TOD, TOM, and SPT can price differently because their settlement dates and funding mechanics differ.

How do business days affect TOD, TOM, and SPT?

Business days affect TOD, TOM, and SPT because settlement can occur only when the relevant calendars support the value date.

The settlement countdown relies exclusively on valid business days rather than a simplistic calendar-day sequence. If a weekend or sovereign holiday unexpectedly intervenes, the target date forcefully shifts forward.

| Calendar Factor | TOD Effect | TOM Effect | SPT Effect |

|---|---|---|---|

| Weekend | May block same-day settlement if not a business day | Pushes next valid date | Pushes spot date |

| Currency Holiday | Can prevent settlement | Can shift next-day value date | Can shift spot value date |

| Cut-Off Time | Very important | Important | Less compressed |

| Currency Pair | Must support same-day settlement | Must support next-day settlement | Must support spot-date calculation |

Why do weekends matter?

Weekends matter because settlement generally requires valid business days. If the mathematical target day is strictly not a valid operating day, the scheduled value date systematically may shift heavily forward. CME’s EBS value-date calendar material treats weekends and currency holidays as factors in value-date and settlement-date calculation. [CME Group, EBS Value Date Calendar] This structural adjustment proves that a Friday TOM contract actually settles on Monday, creating a three-calendar-day gap.

Why do currency holidays matter?

Currency holidays matter because they can make a planned value date invalid. If a critical sovereign banking center is closed, the delivery mechanism simply fails. SPT is especially affected when the T+2 calculation unintentionally crosses unexpected holidays, forcing the settlement deeper into the future.

Why do cut-off times matter most for TOD?

Cut-off times matter most for TOD because same-day settlement leaves the shortest processing window. Late-day execution may dangerously not leave enough actionable time for vital funding and complex settlement instructions to fully clear. If the daily operational cut-off is missed by minutes, the TOD trade is structurally impossible to execute.

Business days, holidays, and cut-off times can change whether TOD, TOM, or SPT settlement is actually possible.

How do TOD, TOM, and SPT differ from forwards?

TOD, TOM, and SPT differ from forwards because they sit on or before the spot value-date boundary, while forwards settle beyond spot.

The short-dated contracts are designed to compress or match the immediate delivery window. Conversely, a forward deliberately targets a future horizon vastly extended beyond standard near-term parameters.

| Contract Type | Settlement Timing | Mechanical Category |

|---|---|---|

| TOD | Same-day | Short-dated spot timing |

| TOM | Next business day | Short-dated spot timing |

| SPT | Standard spot date | Spot timing |

| Forward | After spot date | Future-dated contract |

| Swap | Two settlement legs | Rollover or funding structure |

Why are TOD and TOM not automatically forwards?

TOD and TOM are not automatically forwards because they shorten settlement rather than push it beyond spot. TOD and TOM securely settle firmly before or efficiently around the normal spot window. Transactions settled on or before the second business day after the trade date are classified as spot foreign exchange transactions. [Bank of China, 2026]

What makes a forward mechanically different?

A forward is mechanically different because it settles on a future date beyond the Value Spot date. The heavily delayed future date is an intrinsic part of the contract’s strategic purpose. ANZ defines a forward exchange contract as an agreement to exchange one currency for another on a future date beyond the Value Spot date. [ANZ, Introduction to Foreign Exchange]

Where does SPT sit in the boundary?

SPT sits at the standard spot reference point. It serves as the baseline measuring stick. TOD and TOM are mechanically significantly shorter than the SPT baseline. True forward timing essentially begins immediately after the standard spot date entirely, definitively not before it.

TOD, TOM, and SPT are short-dated FX settlement structures, while forwards are future-dated beyond spot.

How do TOD, TOM, and SPT appear on trading venues?

TOD, TOM, and SPT can appear on trading venues as short contract codes that identify settlement timing.

These highly visible shorthand labels elegantly prevent disastrous communication errors exactly when institutional traders furiously execute rapid deals. However, slash-coded formats like TOD/TOM imply a fundamentally different, two-legged structure entirely.

| Code | Typical Meaning | Venue Interpretation |

|---|---|---|

| TOD | Today | Same-day settlement instrument |

| TOM | Tomorrow | Next-day settlement instrument |

| SPT | Spot | Standard spot settlement instrument |

| TOD/TOM | Swap-style pair | Roll today to tomorrow |

| TOM/SPT | Swap-style pair | Roll tomorrow to spot |

Why do venues use short codes?

Venues use short codes to identify settlement timing quickly. TOD, TOM, and SPT easily can effortlessly appear precisely as concise instrument codes prominently rather than confusingly long, verbose descriptions. Moscow Exchange lists FX instruments using codes such as TOD, TOM, SPT, TOD/TOM, and TOM/SPT. [Moscow Exchange, FX Instruments]

What does TOD/TOM mean mechanically?

TOD/TOM usually describes a two-date structure involving today and tomorrow value dates. It is emphatically not the exact same as a single standalone TOD contract. When venues meticulously label them this exact way, slash-code structures resolutely should definitely be actively read strictly as short-date swap or sophisticated rollover-style structures.

What does TOM/SPT mean mechanically?

TOM/SPT usually describes a two-date structure involving tomorrow and spot value dates. It is definitively wildly different functionally from a simple single TOM or isolated single SPT contract. The visible slash effectively indicates a complex two-date structure explicitly rather than exactly one standalone settlement date.

TOD, TOM, and SPT can appear as venue codes, while TOD/TOM and TOM/SPT usually signal two-date structures.

How do TOD, TOM, and SPT affect operational risk?

TOD, TOM, and SPT affect operational risk by changing how much time exists between trade agreement and settlement.

The aggressive compression of time significantly elevates the probability of catastrophic settlement failure if systems are not perfectly aligned. Each distinct timing code uniquely dictates the level of panic within back-office clearing departments.

| Risk Layer | TOD | TOM | SPT |

|---|---|---|---|

| Funding Readiness | Immediate | Next day | Standard spot window |

| Instruction Risk | Highest pressure | Moderate pressure | Lower timing pressure |

| Calendar Risk | Same-day validity | Next-day validity | Spot-date validity |

| Cut-Off Risk | Very high | Moderate | Lower |

| Settlement Risk | Compressed window | Short window | Standard spot window |

Why is TOD operationally strict?

TOD is operationally strict because settlement is compressed into the trade date. Any unforeseen delay violently inside critical funding operations or complex settlement instructions brutally can quickly become absolutely critical. The margin for error is essentially zero.

Why is TOM less compressed than TOD?

TOM is less compressed than TOD because it gives one business day before settlement. However, TOM undeniably still heavily requires vastly faster preparation comprehensively than standard spot.

Why is SPT operationally easier than TOD or TOM?

SPT is operationally easier than TOD or TOM because it normally provides the standard spot settlement window. The standard spot timing generously gives vastly more time efficiently for necessary funding and robust settlement instruction checks. BIS identifies principal risk, replacement cost risk, and liquidity risk as main FX transaction risks. [BIS, FX Settlement Risk]

TOD, TOM, and SPT affect operational risk by changing how much time exists between trade agreement and settlement.

What examples make TOD, TOM, and SPT easier to understand?

Examples make TOD, TOM, and SPT easier to understand by showing how today, tomorrow, and spot value dates change settlement mechanics.

Practical scenarios perfectly isolate the precise differences effectively without heavily relying purely on abstract theory. They brilliantly demonstrate the harsh mechanical reality dictating daily institutional flow.

| Example Type | What It Shows |

|---|---|

| TOD Example | Trade and settlement happen on same day. |

| TOM Example | Trade today, settle next business day. |

| SPT Example | Trade today, settle on standard spot value date. |

| Friday Example | Weekends change how value dates appear. |

| Holiday Example | Currency holidays can shift value dates. |

| Forward Contrast Example | Future maturity differs from TOD/TOM/SPT. |

What does a TOD example show?

A TOD example shows a contract where settlement is targeted for the trade date. It highlights the urgent demand for immediate, same-day funding readiness. Panin describes Today as foreign-exchange purchase or sale where the delivery date equals the transaction date. [Panin, Today Tomorrow Spot]

What does a TOM example show?

A TOM example shows a contract where settlement is targeted for the next business day. It effectively highlights the rigid T+1 timing gap perfectly. Panin describes Tomorrow as delivery one business day after the transaction date. [Panin, Today Tomorrow Spot]

What does an SPT example show?

An SPT example shows a contract where settlement follows the standard spot value date. It elegantly explains the fundamental difference specifically between rapid spot pricing and literal same-day delivery. Citi describes Value Spot as settlement on the second business day from the trade date. [Citi, FX Transactions]

Examples show that TOD, TOM, and SPT are mainly value-date differences: today, tomorrow, and spot.

How should readers interpret TOD, TOM, and SPT correctly?

Readers should interpret TOD, TOM, and SPT through value date, settlement gap, contract code, and trade confirmation.

While the bold three-letter code is undeniably useful as rapid shorthand, the specific value date exclusively confirms exactly whether same-day, next-day, or standard spot timing genuinely applies. Do not erroneously assume absolutely all FX contracts use identical settlement timing. Slashes indicate vastly different two-date structures.

| Interpretation Layer | Reader Question |

|---|---|

| Contract Code | Is the label TOD, TOM, SPT, TOD/TOM, or TOM/SPT? |

| Trade Date | When was the deal agreed? |

| Value Date | When is settlement scheduled? |

| Settlement Gap | Is it T+0, T+1, or standard spot? |

| Business-Day Calendar | Are weekends involved? |

| Holiday Calendar | Are currency holidays involved? |

| Slash-Code Check | Is it standalone or two-date? |

| Forward Boundary | Is the date beyond spot? |

| Trade Confirmation | What final terms control the contract? |

Which field should be read first?

The value date should be read first because it proves the settlement mechanics. While the contract code is incredibly useful, the formal value date flawlessly confirms exact same-day, next-day, or standard spot timing.

What should readers not assume?

Readers should not assume all FX contracts use the same settlement timing. Distinct TOD, TOM, and SPT prices are definitively absolutely not automatically mathematically identical. Furthermore, slash-code contracts like TOD/TOM are completely not the exact same functionally as standalone single-date contracts.

Where does final interpretation come from?

Final interpretation comes from product type, contract code, trade date, value date, pair convention, and trade confirmation. Contract labels overwhelmingly are merely convenient shorthand, absolutely not legally binding substitutes for the actual printed terms.

TOD, TOM, and SPT should be interpreted through value date, settlement gap, contract code, and trade confirmation.

What mistakes cause confusion about TOD, TOM, and SPT contracts?

Most confusion comes from reading TOD, TOM, and SPT as price labels instead of settlement-date mechanics.

Treating SPT as same-day delivery

Mistake: The reader assumes SPT means immediate settlement.

Correction: SPT usually means standard spot value-date settlement, not same-day TOD settlement. [Citi, FX Transactions]

Treating TOD and TOM as forwards

Mistake: The reader assumes any timing code other than SPT must be forward-based.

Correction: TOD and TOM are shorter value-date structures, not future-dated forwards. [Bank of China, 2026]

Ignoring pricing adjustment

Mistake: The reader assumes TOD, TOM, and SPT must all have the same rate.

Correction: Settlement timing can affect the all-in rate, and same-day or next-day settlement may factor swap interest rate into price. [Citi, FX Transactions]

Confusing standalone contracts with slash contracts

Mistake: The reader treats TOD/TOM as the same as TOD.

Correction: A slash-code structure usually involves two settlement dates, not one standalone value date.

Ignoring business-day calendars

Mistake: The reader counts ordinary calendar days.

Correction: FX settlement uses valid business days and can be affected by currency holidays. [CME Group, EBS Value Date Calendar]

Most confusion comes from reading TOD, TOM, and SPT as price labels instead of settlement-date mechanics.

Which terms confirm whether a contract is TOD, TOM, or SPT?

TOD, TOM, and SPT are confirmed through contract code, trade date, value date, settlement cycle, pair convention, and trade confirmation.

These terms seamlessly interlock to definitively map the chronological lifecycle of the trade. If any of these fields contradict the basic three-letter code, the explicit dates overwhelmingly govern the true settlement parameters.

| Confirmation Term | What It Confirms |

|---|---|

| Contract Code | TOD, TOM, or SPT label. |

| Trade Date | When the deal is agreed. |

| Value Date | When settlement is scheduled. |

| Settlement Cycle | T+0, T+1, or standard spot. |

| Pair Convention | Whether the pair has special timing. |

| Holiday Calendar | Whether value date is valid. |

| Cut-Off Time | Whether same-day settlement is possible. |

| All-In Rate | Whether timing adjustment may be included. |

| Trade Confirmation | Final agreed terms. |

Which terms prove TOD?

Contract code, trade date, and value date prove TOD. If trade date and value date are the same, the contract is mechanically T+0. Value Today descriptions identify same-day settlement as a distinct timing structure. [Citi, FX Transactions]

Which terms prove TOM?

Contract code, trade date, and value date prove TOM. If value date is one business day after trade date, the contract is mechanically T+1. Value Tomorrow descriptions identify next-day settlement as distinct from Value Spot. [Citi, FX Transactions]

Which terms prove SPT?

Contract code, trade date, and value date prove SPT. If value date follows the standard spot convention, the contract is mechanically SPT. Value Spot descriptions commonly define the spot date as the second business day from trade date. [Citi, FX Transactions]

TOD, TOM, and SPT are confirmed through contract code, trade date, value date, settlement cycle, pair convention, and trade confirmation.

What should be validated before interpreting TOD, TOM, and SPT?

Before interpreting TOD, TOM, and SPT, readers should validate contract code, currency pair, trade date, value date, calendars, pricing adjustment, and trade confirmation.

Treating these codes simply as abstract prices entirely ignores their profound logistical impact. Validation vigorously protects against devastating liquidity failures caused by severely mismatched settlement assumptions.

| Validation Question | Pass Condition |

|---|---|

| What is the contract code: TOD, TOM, or SPT? | Code is identified. |

| What is the currency pair? | Pair is clear. |

| What is the trade date? | Deal date is known. |

| What is the value date? | Settlement date is known. |

| Does value date equal trade date? | TOD/T+0 is possible. |

| Does value date fall one business day after trade date? | TOM/T+1 is possible. |

| Does value date follow standard spot timing? | SPT is possible. |

| Is the contract standalone or slash-coded? | Single-date vs two-date structure is clear. |

| Are weekends involved? | Business-day adjustment is checked. |

| Are currency holidays involved? | Holiday adjustment is checked. |

| Is same-day settlement still possible under cut-off time? | TOD feasibility is checked. |

| Does the all-in rate include a timing adjustment? | Pricing treatment is checked. |

| Is the contract actually a forward or swap instead? | Product boundary is checked. |

| Does the trade confirmation support the label? | Final terms confirm classification. |

Which validation question should come first?

The first validation question should confirm the contract code. The contract code frames the settlement label. The value date then proves the mechanics.

Which validation question separates standalone from slash-coded contracts?

The slash-code question separates standalone contracts from two-date structures. TOD/TOM and TOM/SPT should not be read as single-date TOD, TOM, or SPT contracts. Slash-coded structures may signal rollover or swap-style mechanics.

Which validation question separates TOD/TOM/SPT from forwards?

The forward-boundary question separates short-dated spot timing from future-dated contracts. Forwards settle beyond the spot value date. A forward exchange contract exchanges currencies on a future date beyond the Value Spot date. [ANZ, Introduction to Foreign Exchange]

Validation should confirm whether the contract is TOD, TOM, SPT, slash-coded, forward-based, or swap-like before interpreting settlement mechanics.

Conclusion

TOD, TOM, and SPT contracts differ mechanically through value date, not currency-pair identity.

TOD targets same-day settlement, TOM targets next-business-day settlement, and SPT targets the standard spot value date. Citi separates Value Today, Value Tomorrow, and Value Spot as different FX settlement timing structures. [Citi, FX Transactions]

A TOD, TOM, or SPT contract should be interpreted through its value date, settlement gap, contract code, calendar rules, pricing treatment, and trade confirmation before assuming how the FX settlement will occur.

Frequently Asked Questions

What does TOD stand for in forex?

TOD stands for ‘Today’ or ‘Value Today’. It means the currency exchange settles on the exact same day the trade is executed (T+0), requiring immediate funding readiness.

How is TOM different from SPT?

TOM (Tomorrow) settles one business day after the trade date (T+1), providing a brief operational window. Conversely, standard SPT (Spot) typically settles two business days after the trade date (T+2).

Why would a trader use a TOM/SPT contract?

A TOM/SPT contract is a short-dated swap that rolls an exposure from tomorrow to the standard spot date. It is often used to push immediate settlement obligations forward by one day without taking on long-term forward risk.

Do weekends affect TOM and SPT settlement?

Yes. Forex settlement strictly counts valid business days. If a TOM or SPT settlement date lands on a weekend or a recognized currency holiday, the actual value date is pushed to the next valid business day.