Why Does an NDF Avoid Physical Delivery of the Local Currency?

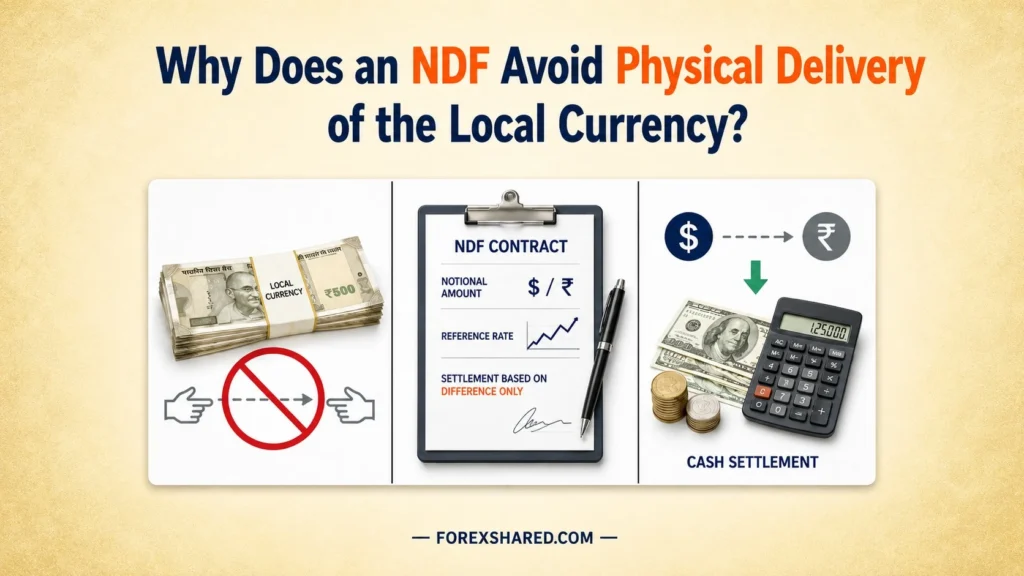

An NDF avoids physical delivery of the local currency because it is designed for markets where the local currency may be restricted, non-convertible, difficult to transfer offshore, or impractical to deliver through normal settlement channels. Instead of engaging in complex onshore logistics, counterparties agree to settle the contract's outcome entirely in a universally accessible proxy asset.

The Non-Deliverable Forward (NDF) directly references the local currency's exchange rate, effectively providing complete exposure to its macroeconomic movement. However, at maturity, it structurally bypasses the actual exchange of principal sums. Settlement occurs strictly through a net cash settlement payment formulated in a highly liquid settlement currency, usually United States Dollars (USD).

NDFs act as contracts for the difference between an agreed exchange rate and the spot rate at maturity, settled through a single proxy payment without funding in the underlying currencies (BIS).

This article is educational only and does not constitute financial advice. Trading foreign exchange on margin carries a high level of risk.

What does “no physical delivery” mean in an NDF?

“No physical delivery” means the underlying local currency is not exchanged at maturity, even though the contract still references that currency’s exchange-rate movement. A firm grasp of NDF contract structure necessitates clearly separating the asset that dictates the economic exposure from the asset actually used to execute the final payment.

Which currency is avoided at settlement?

The currency avoided at settlement is the local or restricted currency referenced by the NDF. The contract deliberately bypasses any requirement to transfer or receive the restricted asset onshore. This intentional absence of gross principal exchange is precisely the mechanism that makes the forward technically "non-deliverable."

What still connects the contract to the local currency?

The contract remains connected to the local currency because the local currency’s exchange-rate movement determines the cash-settlement result. The initial agreed-upon exchange rate and the final market fixing rate are both explicitly calculated in terms of the restricted currency. The economic exposure remains fully intact.

Where does the settlement actually happen?

Settlement happens through a separate payment currency rather than through transfer of the restricted local currency. Upon maturity, the entire economic difference between the inception rate and the terminal spot rate is mathematically converted and wired utilizing an offshore banking channel.

“No physical delivery” means the NDF references the local currency but settles the economic difference without transferring that currency.

Why do restricted currencies make delivery difficult?

Restricted currencies make delivery difficult when local rules, convertibility limits, or offshore transfer barriers prevent normal currency settlement. Non-delivery structurally solves a profound access dilemma; counterparties invent workarounds because onshore execution is legally prohibited or economically unviable. Grasping Local delivery restrictions validates why derivatives markets evolved to bypass sovereign bottlenecks.

Which restriction blocks normal forward delivery?

Normal forward delivery can be blocked when the local market restricts currency conversion, offshore transfer, or access to settlement systems. Capital controls deliberately restrict the free movement of money across borders, preventing foreign banks from securing the required local-currency reserves necessary to satisfy standard gross obligations.

Where does the offshore participant face the delivery gap?

The offshore participant faces the delivery gap when it has economic exposure to the currency but lacks practical access to local settlement. A multinational corporation receiving revenue in a restricted jurisdiction may desperately require hedging protection, but cannot legally open the domestic banking channels necessary to process a traditional forward contract.

What makes non-delivery useful under capital controls?

Non-delivery is useful under capital controls because it allows economic exposure management without moving the restricted currency across the delivery channel. Sidestepping physical delivery nullifies the legal barrier. Counterparties effectively agree to a side-bet executed in an unrestricted zone, perfectly mirroring the onshore financial risk.

NDFs avoid local-currency delivery because restricted currencies can make normal offshore delivery unavailable, limited, or operationally difficult.

How does cash settlement replace local-currency delivery?

Cash settlement replaces local-currency delivery by comparing the agreed NDF rate with a later fixing or reference rate and settling only the net difference. By entirely neutralizing the logistical requirement to mobilize gross principal, the trade safely converts abstract rate volatility into a precise, highly liquid financial payout.

Which rate anchors the contract at the start?

The agreed NDF rate anchors the contract at the start because it sets the forward reference point for later settlement. When counterparties enter the trade, they mathematically lock in a distinct expectation of future value. This static parameter provides the definitive baseline against which terminal reality will be relentlessly judged.

Where does the fixing rate replace delivery?

The fixing rate replaces delivery by providing the final market reference used to determine the cash-settlement outcome. Observed at a designated temporal checkpoint prior to maturity, this official market data entirely dictates whether the contract generates a net gain or a net liability.

What makes the payment “net” instead of deliverable?

The payment is “net” because only the difference is settled, not the full currency amounts. Net settlement guarantees that if a ten-million-dollar notional position experiences a fractional deviation yielding a fifty-thousand-dollar variance, only the fifty-thousand-dollar difference is physically wired.

Cash settlement replaces local-currency delivery by paying only the economic difference in a tradable settlement currency.

Why is the settlement currency usually separate from the local currency?

The settlement currency is usually separate from the local currency because the NDF needs a payment currency that both parties can actually deliver and receive. If the operational restriction natively prevents onshore liquidity clearing, mandating compensation in that same blocked asset defies structural logic. Establishing Proxy-currency cash settlement ensures execution viability.

Which problem does the settlement currency solve?

The settlement currency solves the payment problem by giving both parties a tradable currency for the final cash settlement. Utilizing USD effortlessly neutralizes cross-border paralysis, guaranteeing smooth, frictionless resolution across universally accepted correspondent banking structures.

What stays local even when payment is offshore?

The economic exposure stays local because the restricted currency’s exchange-rate movement still drives the settlement outcome. Even though the payout manifests in a foreign denomination, the volatility profile perfectly traces the domestic pricing shifts.

Where can confusion appear for readers?

Confusion appears when readers assume that settlement in another currency means the local currency no longer matters. Counterparties receive compensation in dollars, but their financial fate is tethered strictly to the restricted currency's dynamic market performance.

The settlement currency is separate because the NDF needs a practical payment currency while still referencing the local currency’s exchange-rate movement.

When is avoiding physical delivery most useful?

Avoiding physical delivery is most useful when the user needs economic exposure to a local currency but cannot, should not, or does not need to receive or deliver that currency. For institutional operators seeking robust protection, forcing localized infrastructure frequently triggers severe legal and logistical burdens.

When does a company need exposure without receipt of currency?

A company may need exposure without receipt of currency when it faces local-currency risk but does not need to physically hold that currency offshore. An entity generating substantial revenues inside a restricted zone utilizes offshore hedging purely to offset anticipated depreciation losses without dragging trapped capital backward across strict borders.

Where does an investor benefit from non-delivery?

An investor may benefit from non-delivery when direct local-currency access is limited but exchange-rate exposure still matters. Speculators desiring macro participation simply leverage NDFs to execute their thesis cleanly, disregarding onshore banking hurdles.

Which situation still needs a deliverable forward instead?

A deliverable forward fits better conceptually when the user actually needs to receive or pay the underlying currency. If operational supply chain logistics strictly require paying international suppliers with actual capital, an NDF is structurally inadequate. Validating requirements separates protective coverage from procurement necessity.

Avoiding physical delivery is most useful when the user needs economic exposure to a local currency but cannot or does not need to deliver the currency itself.

How does non-delivery change the difference between NDFs and deliverable forwards?

Non-delivery changes the difference between NDFs and deliverable forwards by replacing actual currency exchange with net cash settlement. Both distinct instruments originate from an identical forward pricing base; their terminal conditions forge the primary architectural split.

| Contract Type | What Happens at Maturity | Local-Currency Delivery |

|---|---|---|

| Deliverable Forward | Agreed currencies are exchanged | Required |

| NDF | Net difference is cash-settled | Avoided |

Which contract transfers the underlying currency?

The deliverable forward transfers the underlying currencies, while the NDF does not transfer the restricted local currency. A standard forward forces physical gross alignment, shifting genuine capital across ledgers.

What does the NDF keep from the forward structure?

The NDF keeps the forward-style rate agreement and exchange-rate exposure but changes how the contract settles. Traders retain precise future-valuation stability without adopting unmanageable delivery obligations.

Where does pricing become secondary in the comparison?

Pricing becomes secondary when the reader has not yet identified whether the contract delivers currency or settles in cash. It is utterly irrelevant if the forward rate appears highly attractive if your corporate entity possesses zero legal authority to clear the asset physically.

NDFs differ from deliverable forwards because they keep the forward exposure but remove the physical delivery obligation.

What risks are reduced when the local currency is not delivered?

When the local currency is not delivered, the contract can reduce local-currency transfer burdens, but it does not remove market, counterparty, or fixing-related risk. Bypassing delivery reallocates vulnerability rather than annihilating it completely.

Which operational burden becomes lighter?

The operational burden becomes lighter because the parties do not need to exchange the full local-currency amount. Managing stringent administrative logistics across multiple sovereign banking regimes is effortlessly sidestepped.

What risk remains even without delivery?

Exchange-rate risk, counterparty risk, and settlement-performance risk remain even when the local currency is not delivered. A non-delivery framework does not protect against aggressive market movement, nor does it guarantee the other party will actually furnish the net USD payout.

Where does non-delivery create a new dependency?

Non-delivery creates a new dependency on the fixing mechanism because the final cash payment depends on the chosen reference rate. Exchanging physical delivery risk effectively injects basis risk if the external reference index becomes manipulated, disrupted, or substantially divergent from actual onshore parity.

Avoiding physical delivery reduces local-currency transfer burdens, but it does not remove market, counterparty, or fixing-related risk.

What examples make no-local-currency delivery easier to understand?

Examples make no-local-currency delivery easier to understand when they show the difference between economic exposure and actual currency transfer. Illuminating these dynamics strips away complex terminology, validating practical mechanics.

What does a restricted-currency hedge reveal?

A restricted-currency hedge reveals how an NDF can reference a currency that is difficult to deliver offshore. By anchoring the calculation strictly to domestic value while securing execution in dollars, participants perfectly neutralize localized depreciation threats.

What does a deliverable-forward contrast reveal?

A deliverable-forward contrast reveals that a standard forward completes through currency exchange, while an NDF completes through cash settlement. Both secure a future rate, but only one guarantees physical capital repossession at terminal dates.

Where does the settlement-currency example help?

The settlement-currency example helps by showing how the contract can close without transferring the restricted local currency. It clarifies why USD assumes the role of execution proxy to enforce compensation safely regardless of underlying sovereign blockades.

Examples show that an NDF avoids local-currency delivery while still preserving exposure to the local currency’s exchange-rate movement.

What mistakes cause readers to misunderstand non-delivery?

Readers misunderstand non-delivery when they confuse economic exchange-rate exposure with physical currency transfer. Addressing these conceptual flaws drastically tightens structural comprehension.

Assuming “non-deliverable” means no currency exposure

Mistake: The reader thinks no delivery means the local currency is irrelevant.

Correction: The local currency still drives the contract outcome through the fixing rate, dominating the financial result.

Treating cash settlement as actual currency exchange

Mistake: The reader assumes the cash payment is the same as receiving or delivering the local currency.

Correction: Cash settlement transfers only the net difference, not the underlying currency amount.

Ignoring the settlement currency

Mistake: The reader focuses only on the restricted currency.

Correction: The settlement currency is the vital payment route that explicitly makes non-delivery functionally operable.

Comparing NDFs and forwards before checking delivery

Mistake: The reader compares rates first.

Correction: Delivery structure must definitively be checked before pricing or risk comparison begins.

Most misunderstanding comes from confusing economic exposure with physical currency delivery.

How can readers fix confusion about no-local-currency delivery?

Readers can fix confusion about no-local-currency delivery by separating the currency that creates exposure from the currency used for settlement. Cleaving these dynamics precisely eliminates subsequent misreadings of derivative architecture.

What should be read first in the contract terms?

The settlement clause should be read first because it reveals whether the contract ends in delivery or cash settlement. This fundamental binary securely outlines every subsequent strategic step.

Which words signal that delivery is avoided?

Words such as non-deliverable, fixing date, settlement currency, cash settlement, and reference rate often signal that delivery is avoided. Immediately identifying these markers protects traders from anticipating physical receipt.

Where should the reader separate exposure from payment?

The reader should separate exposure from payment by identifying the local currency as the reference exposure and the settlement currency as the payment route. This duality forms the absolute heartbeat of off-shore liquidity.

The cleanest fix is to separate the currency that creates exposure from the currency used for settlement.

What should be validated before interpreting no-delivery in an NDF?

Before interpreting no-delivery in an NDF, readers should confirm whether the contract references a local currency without requiring that currency to be physically exchanged.

The biggest mistake is assuming that a contract referencing a currency must also deliver that currency. A better approach is to treat an NDF as an instrument that captures local-currency exposure but settles that exposure through an offshore, non-deliverable cash payment.

Non-Delivery FAQs

Why would someone want an NDF if they don't get the actual currency?

Because they are using it purely as a financial hedge against price fluctuations, rather than for purchasing supplies. The net cash settlement perfectly offsets their onshore losses without forcing them to navigate complex international banking hurdles.

Are NDFs only settled in USD?

No. While USD is heavily utilized because it is a globally liquid standard, counterparties can technically agree to settle the net difference in Euros, Japanese Yen, or any other freely convertible settlement currency depending on their mutual liquidity preferences.

Does avoiding physical delivery mean there is no counterparty risk?

Absolutely not. You are still completely reliant on the other institution's ability and willingness to wire the net cash difference on the settlement date. If they default, you absorb the financial loss just as you would with a deliverable forward.